The start of a new year often brings with it a wave of changes to key financial figures that can impact your retirement savings, taxes, and overall financial well-being. 2025 is no exception. Let's check out some of the more important updates that could affect your finances in the new year.

Retirement Savings

Good news for you savers out there! The 401(k) contribution limits have increased, allowing you to potentially maximize your retirement contributions. For 2025, the maximum employee contribution limit for 401(k) plans has risen to $23,500 up from the 2024 amount of $23,000. This increase could provide an opportunity to boost your retirement savings.

This year also brings the introduction of "Super Catch-Up" contributions, a valuable (but not new) option for those aged 50 and older. For 401(k) and 403(b)plans, the deferral limit is the greater of $5,000 or 150% of the normal “age 50” catch-up contribution for 2025 - $7,500. So, the super catch-up would equal 150% x $7,500 which is $11,250.

The SIMPLE IRA super catch-up is right long those same lines. The greater of $5,000 or 150% of the 2025 regular “age 50” catch-up limit for SIMPLE IRAs being $3,500, could potentially give you a super catch-up of $5,250 (150% x $3,500).

There is also now a “Super Catch-Up” exclusively for those aged 60-63, which is $11,250 for a total maximum of $37,750. Note that the catch-up limit oddly drops back down at 64.

Tax Considerations

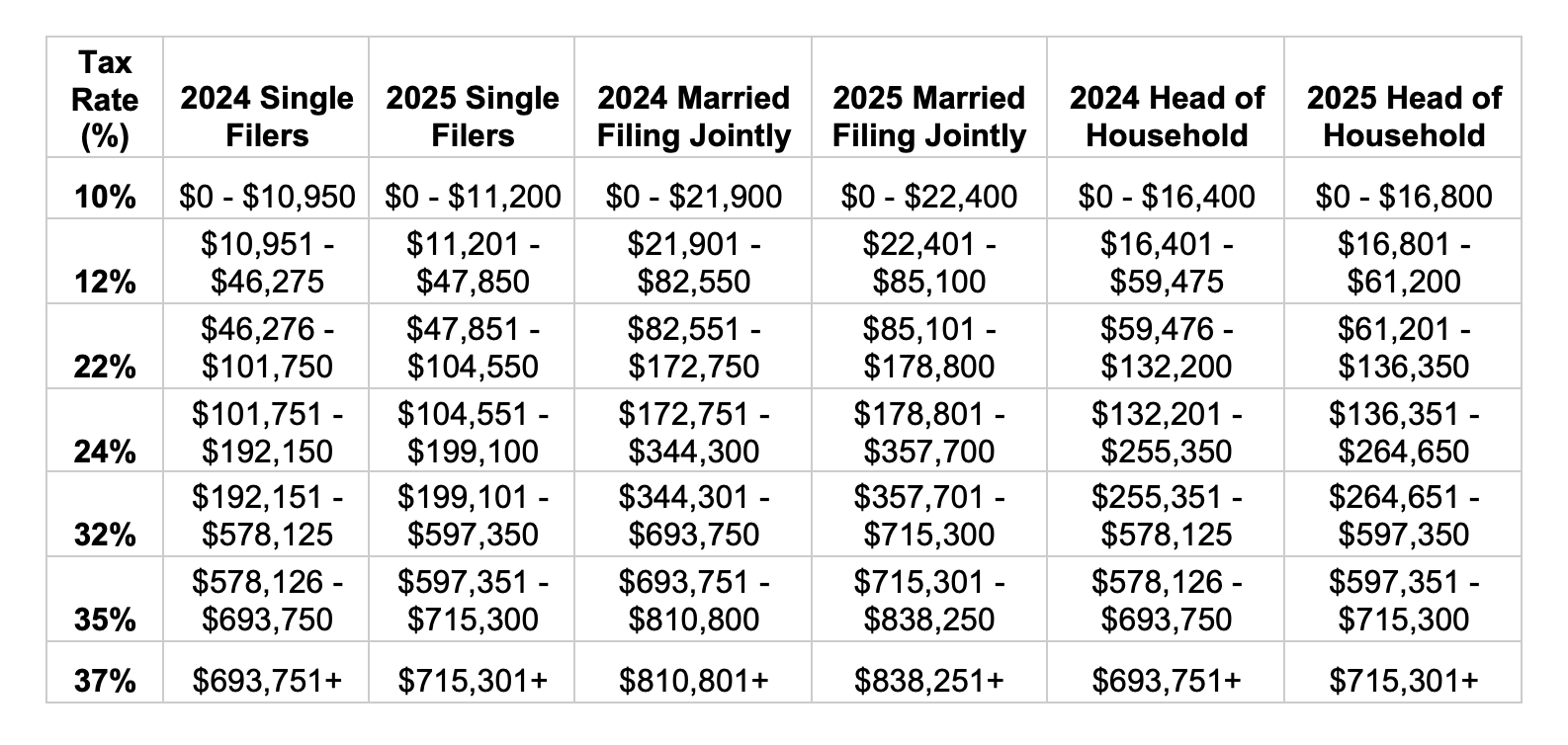

The 2025 tax brackets have been adjusted to account for inflation. The percentage brackets are the same, but the income ranges have shifts. The income levels at which you move into higher tax brackets have increased.

While this may seem like good news, it's important to consult with a tax professional to optimize your tax strategy. They can help you identify potential deductions and credits that can minimize your tax liability.

Note: The annual gift tax exclusion has also risen to $19,000 in 2025 (from $18,000 in 2024) allowing you to gift larger amounts to loved ones, such as family members or charities, without incurring gift tax consequences.

Social Security and Healthcare

The 2025 Social Security Cost-of-Living Adjustment (COLA) is 2.5%, slightly lower than the previous year's 3.2%, primarily because the inflation has cooled down. While this provides a modest increase to Social Security benefits, it helps to offset the ongoing impact of inflation on the purchasing power of these benefits.

However, the monthly premium for Medicare Part B has increased to $185. This is a $10.30 increase from 2024 brought about by projected price changes and assumed increases in overall medical care that have historically occurred. The increase will likely impact the out-of-pocket healthcare expenses for Medicare beneficiaries.

High Earners

High earners now have access to higher annual contribution limits for defined contribution plans, such as 401(k)s and 403(b)s. The per-compensation plan total contribution limit, which represents the maximum annual contribution for these plans, has increased to $70,000 from $69,000 in 2024, providing greater flexibility for high earners to maximize their retirement savings contributions.

Navigating the Changes

These changes highlight the importance of staying informed about evolving financial regulations and their potential impact on your personal finances.

- Review and Adjust: Evaluate your current retirement savings strategy and make adjustments as needed to take advantage of the increased contribution limits. Consider increasing your 401(k) contributions and explore the "Super Catch-Up" option if eligible.

- Tax Planning: Consult with a qualified tax advisor to discuss your tax situation and explore strategies to minimize your tax liability. They can help you identify potential deductions, credits, and tax planning opportunities that can maximize your after-tax income.

- Understand Medicare Costs: Review your Medicare coverage and understand the implications of the increased Part B premium on your healthcare budget. Explore options to minimize your out-of-pocket costs, such as enrolling in a Medicare Advantage plan or utilizing prescription drug coverage.

By staying informed and proactive, you can effectively navigate these changes and work towards achieving your long-term financial goals. Talk with a member of the SKG Team to learn how.

Representatives do not provide tax and/or legal advice. Any discussion of taxes is for general informational purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax or accounting advice. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

CRN202712-7919597