Dubbed a “silent killer” of retirement cash flow, Medicare's Income-Related Monthly Adjustment Amount (IRMAA) can have a major effect on your social security income and IRA withdrawals in retirement. Your Medicare Part B premiums are based on your Modified Adjusted Gross Income (MAGI) from two years prior.

If you’ve received a letter and were surprised that your 2025 Medicare Part B and D premiums have gone up, you need to go back to your 2023 MAGI to get an idea of why you’ll be paying more. This may come as a shock to you, plus you might incur a cost that you haven’t budgeted for. Don’t let this catch you off-guard. Understanding IRMAA is vital for managing your post-retirement healthcare costs.

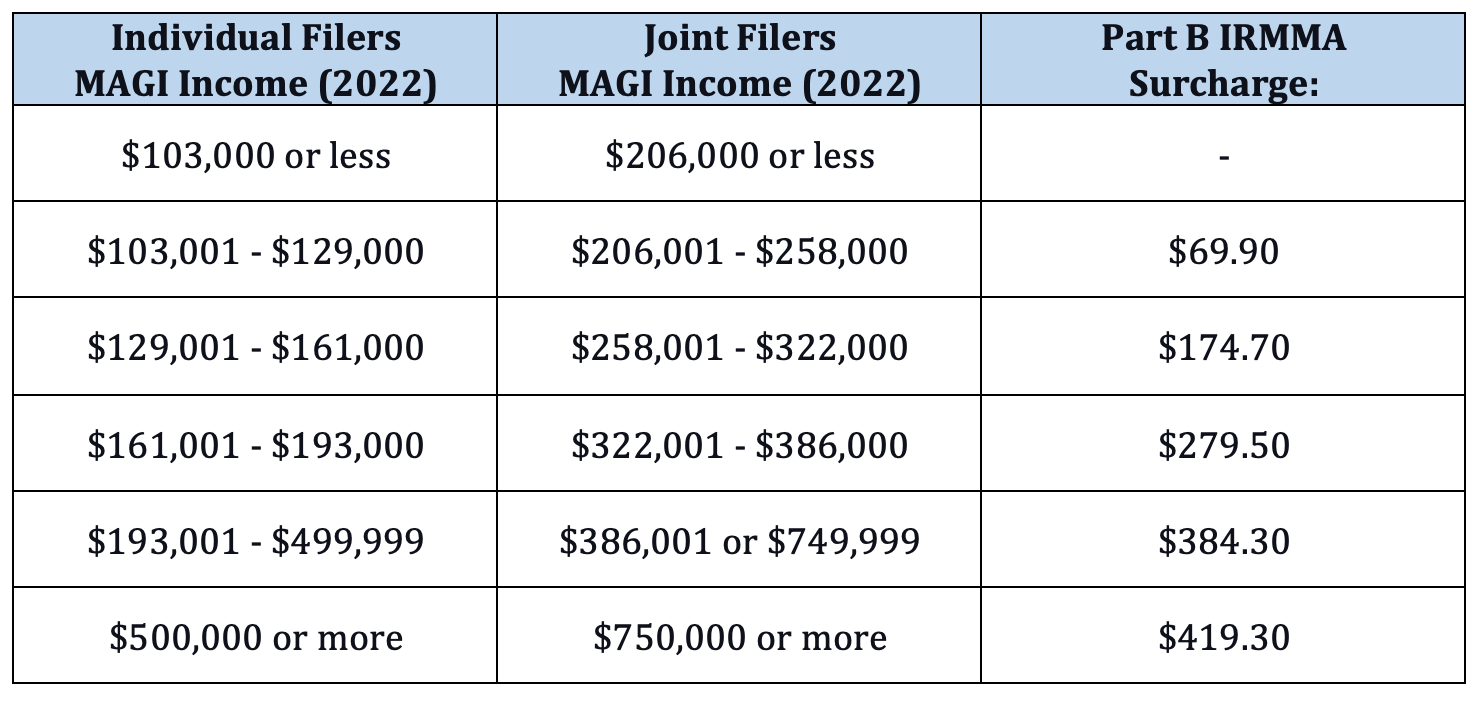

How IRMAA Influenced Medicare Payments in 2024

As we’ve already laid out, the 2024 IRMAA Medicare costs came from income levels reported, two years ago, on the 2022 tax return. Individual earners with an income of $103,000 or less or joint filers reporting $206,000 or less had no additional charge for Medicare Part B or Part D.

The chart below highlights the brackets that were affected.

Solutions to Paying Less

At the heart of how to pay less for Medicare Part B is to control your taxable income. Consider managing taxable items such as Social Security benefits, 1099 income, and withdrawals from IRAs or 401(k) plans to keep your MAGI within the thresholds that qualify for lower Medicare Part B premiums.

Build up your post-tax accounts during your working years

Often, we’re conditioned to save as much as possible into our 401k and also save as much as possible in taxes because we’re doing so on a pre-tax basis. By building up your cash reserves and after-tax brokerage accounts, you can provide yourself tremendous flexibility for later. This is called tax diversification. Remember, when you withdraw money from a brokerage account, you’re only taxed on your gains, not your cost basis, which makes this much more tax efficient than a pre-tax 401k.

Build up your tax-advantaged accounts during your working years

This same logic extends to tax-advantaged accounts and investments. For example, municipal bonds create tax-free interest and loaning against a life insurance policy can also help you to avoid taxation. The Roth 401k and IRA are also accounts that — if invested into early and left to grow — can provide important sources of capital and income without triggering an impact on your Medicare premiums.

Social Security Benefits

Delaying the start of your social security benefits will help reduce your overall income, lowering your MAGI in your early retirement years. But the longer you wait, the larger your monthly benefit becomes, so getting ahead of the game is important. One way to push back that start-date on your benefits, is finding money from alternative sources like a savings account or taking on part-time employment.

1099 Income

If you’re self-employed or receive income through 1099s, take advantage of all available business deductions. Keep detailed records of business-related expenses to lower your taxable income. Work with a tax professional to identify tax-saving opportunities. For instance, contributing to a retirement account like a Simplified Employee Pension (SEP) IRA or a Solo 401(k) plan is one way to reduce your taxable income. Also, remember, that interest collected from bank accounts and bonds as well as passive investments will generate a 1099.

Withdrawals from IRAs or 401(k) plans

Consider gradually converting traditional IRA or 401(k) funds into Roth IRAs. Roth conversions may be taxable events, but they can help reduce future taxable income. Plan your withdrawals strategically to minimize tax liability. For example, withdraw funds from taxable accounts first and let your tax-advantaged retirement accounts continue to grow tax-deferred. Combining Roth conversions with delaying social security and the use of after-tax investments can really create optionality later in life.

Work Stoppage Events

One of the most common instances where you might find your IRMAA too high to afford, is when a work stoppage event occurs. For instance, if you left your job in 2024, but your 2025 Medicare Part B payment is based on your 2023 MAGI, when you were employed. Now what?

Luckily, there’s an appeals process. You can file an appeal due to job loss or retirement to adjust your Medicare Part B payment to align your costs with your current financial circumstances. Note, that it’s not uncommon to have to appeal the appeal. If your appeal is justified don’t give up on the first denial!

Other appealable reasons:

Work stoppage is the most common reason for an appeal, but here are other valid reasons Medicare will consider:

- The death of a spouse

- Marriage

- Divorce or annulment

- Involuntary loss of income-producing property due to a natural disaster, disease, fraud, or other circumstances

- Loss of pension

- Receipt of settlement payment from a current or former employer due to the employer’s closure or bankruptcy

Work With the SKG Team

Effective tax planning is crucial for grasping IRMAA's influence on healthcare costs. Professional wealth management experts from the SKG team excel in integrating tax planning into your financial strategy. Our expertise empowers retirees to navigate the intricacies of IRMAA and other financial aspects, ultimately optimizing their post-retirement financial well-being.

Representatives do not provide tax and/or legal advice. Any discussion of taxes is for general informational purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax or accounting advice. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

CRN202705-7414432